Much to my disappointment I ended up owing taxes when I filed my tax return this year. Or said another way I had a tax liability to the IRS.

While paying taxes I legally owe is not itself a bad thing, after all I did not give an interest free loan to Uncle Sam, what really hurts is that if I had undertaken a few actions earlier in the year I could have avoided or significantly reduced my tax bill.

Furthermore avoiding tax liabilities, which you can find on lines 37 (amount you owe) and 38 (penalty on late estimated payments) of your 1040 tax form, can also ensure you don’t end up paying any penalties for overdue or underpaid estimated taxes.

The following tax reduction strategies are simple, possibly good investments and ones that you can put in place today to ensure you only pay what you owe and avoid tax liabilities that lead to penalties – which I call a tax on taxes.

Get your biggest tax refund, guaranteed. Get started today.

401K/IRA Retirement Account Contributions Boost

This is probably the easiest and most effective way to reduce your taxable income because all contributions to a 401K or IRA plan are tax-deductible, as is all the investment growth within the account.

An increase of just a few percent will lower your taxable income (AGI), enabling you to fall into a lower tax bracket and possibly face a much lower tax bill (or refund).

The maximum amount an employee can contribute to a 401(k) has been increasing steadily over the last few years and for individuals over the age of 50, they can make extra catch-up contributions to further lower their taxable income.

So if you can manage it, make a higher retirement savings account contribution during the year or bump up your savings rate as year end approaches. Not only will it reduce your taxable income and bracket, it will help ensure a more comfortable retirement.

Also remember the Required Minimum Distributions (RMDs) are back again for those over 70-1/2 after being paused in 2020. So make sure you take your RMD or face a hefty tax penalty. You can also make a qualified charitable donation (see section below) to meet this requirement.

Itemize to Claim More Deductions

Rather than just take the standard income tax deduction try and itemize your deductions. It may take longer and not as beneficial in years past due to tax law changes, but if you have more than just a straightforward tax situation and/or own property this approach to your taxes could have a big impact on your tax bill.

I know I get about two to three times the standard deduction amount when itemizing my tax deductions. Most leading tax software or an accountant can help you with this for an extra fee, which may be worth it if you get a much larger refund.

Decrease your Paycheck Withholding

A lot of times when a life event occurs, like buying/selling a house or children going to college, folks forget to adjust their employer paycheck withholdings. I learned the importance of understanding this the hard way with a hefty tax bill, due to not withholding enough taxes during the year.

Take the time to ensure that the correct taxes are being withheld so that you don’t have an unexpected tax bill when filing your return. On the flip side, you also don’t want too withhold too much and have a big refund in the subsequent year – because you are just giving a free loan to the IRS.

Using last years returns and various IRS withholding calculators should help you determine the right of amount of taxes to withhold.

Capital Gain Loss Tax Deduction

With most investor portfolio’s facing some level of stock market losses, selling a few loser stocks for a net capital loss is a good way to get a $3,000 (or $1500 for single filers) offset on their income tax return.

So make sure you review your brokerage account statements and tax planning reports. Most now provide a view of your realized and unrealized capital gains, to see what stocks to sell so that you can offset any gains or maximize your capital loss provision.

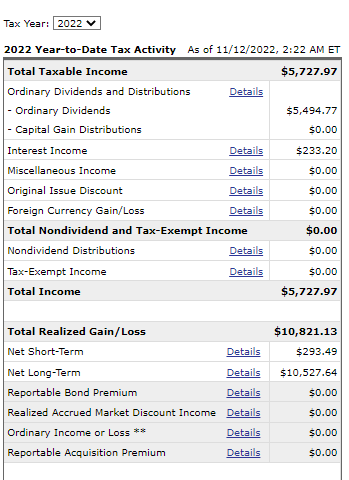

You can see how my YTD tax activity looks on Fidelity below. You will have links to drill down for details and I will definitely be doing some tax loss selling (lots of busted fin-tech shares!). Also don’t forget to factor in dividends, which are taxed as ordinary income.

Investors can carry unused capital losses forward for as long as they live. This means you can recoup some of those losses against future tax returns, and potentially reduce your tax liability for a number of years.

Claim ALL Charitable Donations

Don’t forget that charitable gifts and donations are tax deductible. With the tough economic climate charities are hurting more than ever so help those in need and save some money at tax time to boot.

Remember though, to deduct any charitable donation of money (cash, check, credit or payroll deduction), regardless of amount, a taxpayer must have a bank record or a written communication from the charity (normally a receipt or tax invoice) showing the name of the charity and the date and amount of the contribution.

If you are over 70½, you can make a qualified charitable distribution (QCD) offset your RMD and taxable income. A QCD allows you to transfer up to $100,000 ($200,000 for married couples) each year from your traditional IRAs to your qualified charity of choice.

However you can’t also claim the tax-free transfer as a charitable deduction on Schedule A if you do itemize.

See this post for more details on taxes and forms required around charitable contributions.

Is the $300-$600 charitable deduction available in 2022

Note that the $300 (single filer)/$600 (joint filer), non-itemizer charitable deduction that was provided in the 2021 tax year as part of the COVID stimulus package is no longer available. You will now need to provide receipts for all charitable donations.

Gift Tax Exclusion

It is also a good idea to ensure that any gifts you give are done so before year end so that you and the recipient are covered by the annual federal tax gift exclusion which jumped to $16,000 for 2022 (versus $15,000

in 2021).

Claim Past Stimulus Payments

Many Americans were eligible for claiming one or more economic stimulus tax credits, tax deductions and/or bonus government payments paid over the last few years. These will either reduce your taxable income (deductions) or give you cash back (credits).

So if you haven’t claimed these yet or not sure if you are eligible, make sure you claim these when filing your return for the applicable year.