I am going to take a contrary view of retirement savings and say that in current market conditions you should think about reducing your 401(k) contributions to only invest the amount that is needed to get your company match.

I am normally a strong proponent of company sponsored 401(k)and traditional (IRA) retirement plans because of the tax advantages and long term compounding benefits. However in already volatile markets, that are likely set for further falls in the year ahead, minimizing your 401(k) contributions may be a smarter investment move overall.

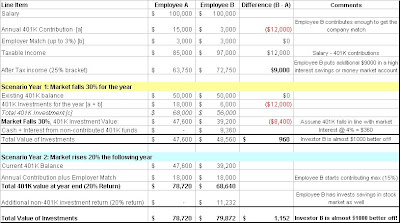

Don’t believe me? Here’s an example using two employees earning $100,000 with different 401(k) contribution levels, and a look at their returns after one year if the market and the value of their investments fall 30% followed by a rise in the subsequent year. To simplify things assume that they have no other investments or deductions.

Get the latest money, tax and stimulus news directly in your inbox

From the above calculations, you can see that Employee/Investor B is almost $1000 better off when the market falls and when the market rises. Now $1000 may not be a lot of money if you are earning $100,000 but it is cash in hand, which can be especially helpful in today’s market environment.

More than stimulus or any other government intervention, 401(k) and retirements funds are the only game in town buying shares today and keeping the market stable.

These retirement funds have to buy stocks to stay in adherence with their plan and asset allocation guidelines. So basically by contributing to your 401(k) you are providing sellers the ability to get rid of their stocks and taking the losses as the market continues to fall.

Without 401(k) plans, the Dow Jones market average would probably be 20 to 30 percent lower today. That’s why investors and Wall street firms should be thanking employees (and not the government) for continuing to contribute to their 401(k) and IRA plans.

I am not suggesting that you stop 401(k) contributions permanently. Once the stock market and the economy stabilizes, you must ratchet those 401(k) investments back up to the maximum and enjoy the benefits of dollar cost averaging and compounding as the prices recover from their lows.

The example above is only a basic guide to illustrate that 401(k) plans aren’t bullet proof and the key, like all your investments, is to take a much more active role in managing your 401(k) in these strange economic times. I know I am.

Editor’s note : Can you spot the assumption I am making in the table above, that would reduce the overall savings to Employee B, but still put him ahead when the market falls?

Your suggestion to pare back on 401K contributions when investment markets are down or volatile is not prudent…The idea is to buy more shares as the market goes down so that when the market stabilizes and rises you have increased your overall portfolio value by taking advantage of the market volatility dips & fluctuations. After all, the 401K is designed for long term investment horizons. Buy low and sell high when you really need the investments to replace your salary income for the rest of your golden years. What are the chances that you will have a Pension plan or Social Security payments coming in to support your lifestyle?

Looking back at this article after a few years, you are spot on Ronaldo and I was wrong to pare back my contributions.

Problem with this chart is it is misleading. WHile the amrket was in tailspin, employee A bought twice a many shares as B and also twice as many than would have been bought be it not for a tailspin. THose who continue to look at 401k’s as mega savings accounts and look at the balance, like the author here, are doomed